What is Black Scholes model?

A Black Scholes calculator answers whether the option is priced fairly. With prices moving every second, "fair" is hard to spot in a sea of live quotes. It's an option pricing calculator that removes the guesswork and gives you a number to check the market price against.

The idea behind it is simple. Price is just probability wearing a price tag. Feed the calculator five market inputs (spot, strike, expiry, interest, and your volatility estimate) and it hands back the option's theoretical value, along with every Greek you need.

Let's read what is a Black Scholes Model/tool and how to use it.

What Is a Black Scholes Calculator?

A Black Scholes calculator runs the Black-Scholes formula for you. Instead of solving the math by hand, you enter five inputs: underlying price, strike, time to expiry, interest rate, and volatility. The calculator returns the fair price for a call or put option.

The model behind the calculator was built by Fischer Black and Myron Scholes in 1973. Robert Merton extended the math soon after. More than 50 years later, it's still the starting point most traders use to sanity check option premiums.

Learn more about Options Trading here

Why Option Traders Use a Black Scholes Calculator

A Black Scholes calculator gives you a closed-form price for calls and puts instantly. That lets you eyeball whether an option looks rich or cheap before you place a trade.

It also does the Greek math for you. Delta, Gamma, Vega, Theta, and Rho show up in the same output table, so you get a full risk picture, not just a price.

This matters most right before high-IV events like earnings or RBI policy days. If the calculator's theoretical price sits well below the live premium, you know you are paying extra for implied volatility, not just time value.

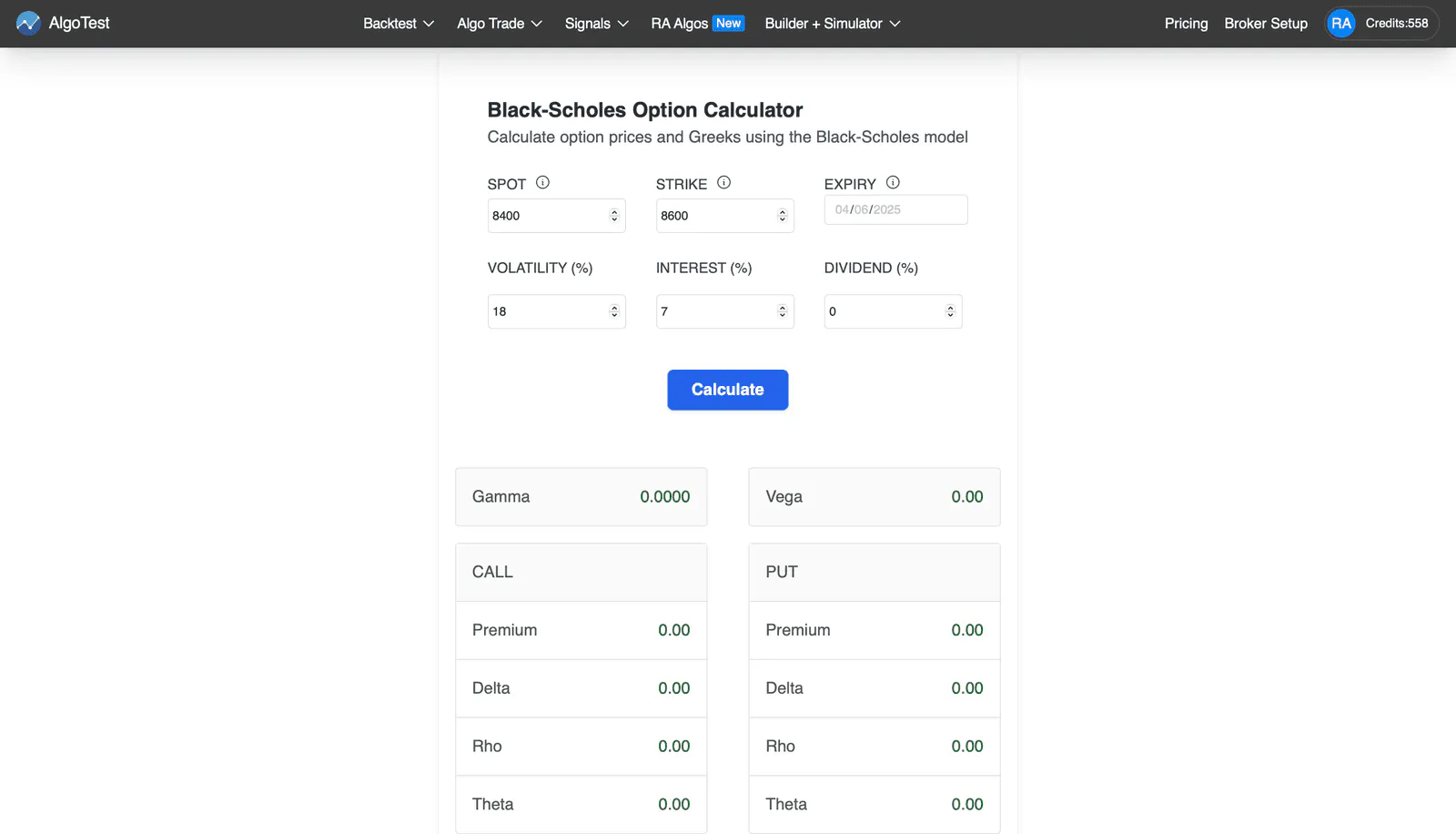

How to use the Black-Scholes tool?

Go to Black Scholes tool on AlgoTest:

SPOT = current underlying price

STRIKE = option’s strike price

EXPIRY = expiration date

VOLATILITY (%) = annualised IV (or your best estimate)

INTEREST (%) = risk-free rate for the option’s tenor

DIVIDEND (%) = expected continuous yield (0 for NIFTY/BANKNIFTY futures)

Click “Calculate.”

Read the output table: you can see call/put premiums and all the greeks.

Change any input and recalculate to see how price and risk metrics move.

Learn how to read and compute implied volatility here

What the Black Scholes Calculator Tells You

→ Theoretical premium: the fair value of the call and put under Black-Scholes assumptions → Delta: how much the price moves for a one-point move in the underlying → Gamma: how fast Delta itself changes → Vega: how sensitive the price is to a change in volatility → Theta: how much value the option loses each day from time decay → Rho: how much the price moves for a change in interest rates

Compare these numbers to the actual market price. A wide gap can point to mispricing, help you build a volatility surface, or tell you how aggressively to hedge a position.

For a worked example with real Nifty numbers, see AlgoTest's guide on how the Black-Scholes model prices option premium.

Limitations to Keep in Mind

A Black Scholes calculator gives you a theoretical price, not a live market quote. Keep a few assumptions in mind before you act on the output:

→ It's built for European-style options, exercised only at expiry (NIFTY and BANKNIFTY options qualify; some stock options don't) → It assumes volatility and interest rates stay constant until expiry, which they rarely do → It doesn't account for transaction costs, bid-ask spreads, or liquidity

Treat the calculator's output as one input in your decision, not the final word on where an option should trade.

If you want to learn about options in detail, check out the financial education section in AlgoTest's documentation.

Join Us as We Simplify Algo Trading in India

You don't need to solve the Black-Scholes formula by hand or guess whether an option is priced fairly. AlgoTest's Black Scholes calculator does that work for you, so you can focus on the trade itself.

Sign up for free and get the full AlgoTest toolkit built for Indian options traders:

→ Backtesting: test your strategy against years of historical data before you risk real money

→ Forward testing: validate the strategy on live market data without any capital at risk

→ Strategy builder: build and customize strategies with a no-code interface

→ Simulator: practice execution in real market conditions using virtual capital

From pricing a single option to running a full strategy, AlgoTest gives you the tools to trade with more confidence and less guesswork.

Other tools