Butterfly Option Strategy: 4 Ways to Build the Same Payoff

The butterfly option strategy is a popular way to trade range-bound markets with defined risk and defined reward. Most traders learn the standard butterfly setup, but few realize that the same payoff can be created using four different option structures.

Each construction has its own advantages, capital requirements, and risk profile before expiry, even though they produce nearly identical outcomes at expiration.

We'll break down the four ways to build a butterfly spread and explain how to choose the right one for your trading style.

What Is a Butterfly Option Strategy?

A butterfly option strategy (or butterfly spread) is a defined-risk, defined-reward, market-neutral options strategy built using three strike prices that are equally spaced apart. It's constructed entirely with calls, entirely with puts, or a mix of both, all expiring on the same date.

Structurally, a butterfly is just two vertical spreads stitched together:

Abull spreadbetween the lowest and middle strike

A bear spread between the middle and highest strike

Combine the two, and you get the strategy's signature shape on a payoff chart: flat near the bottom, rising to a peak at the middle strike, then tapering back down. That tent-like shape, with a body in the middle and wings on either side, is exactly why it's named after a butterfly.

How a Long Call Butterfly Looks in Practice

Take a long call butterfly on NIFTY, three strikes apart and equally spaced:

Buy 1 lower-strike call (e.g., 24,800)

Sell 2 middle-strike calls (e.g., 24,900)

Buy 1 higher-strike call (e.g., 25,000)

This position profits if NIFTY settles near 24,900 at expiry. If NIFTY finishes below 24,800 or above 25,000, the trade incurs a loss, but that loss is capped at the net premium (debit) paid to enter the trade.

There's no scenario where you lose more than what you put in. Remember that each leg here is traded in lots, not individual contracts, so the actual premium paid or received scales with NIFTY's lot size.

The maximum profit is realized if the index expires exactly at the middle strike. The further the price drifts from that point in either direction, the smaller the profit, until it disappears entirely past the outer strikes.

Try AlgoTest Strategy Builder for Free

The Four Ways to Build the Same Butterfly

Most traders learn a butterfly as a single strategy. In reality, the same butterfly payoff can be created using four different option structures.

That's because both the bull spread and bear spread that make up a butterfly can be built using either calls or puts.

At expiry, all four structures produce nearly identical payoff profiles. The reason is put-call parity, which keeps equivalent call and put combinations aligned. If one butterfly structure became significantly cheaper or more expensive than another, arbitrage opportunities would quickly bring prices back in line.

Related: What is Basket Trading

Why Construction Matters

If the payoff is almost identical at expiry, why should you care about the structure?

Because the trading experience before expiry can be very different.

Factors that change across constructions include:

Capital required to enter the trade

Margin blocked by the broker

Early assignment risk on short options

Sensitivity to time decay and volatility changes

For example, an iron butterfly typically requires less upfront capital because it is entered for a credit, while some debit-based butterfly structures can be more capital intensive.

The academically preferred construction combines a call bull spread with a put bear spread. While this structure is often considered cleaner from a theoretical perspective, it usually requires the highest capital outlay.

As a result, most traders prefer simpler and more capital-efficient alternatives such as the all-call butterfly, all-put butterfly, or iron butterfly.

The best structure is not always the one that looks best on paper. It is the one that fits your capital, margin requirements, and trading style.

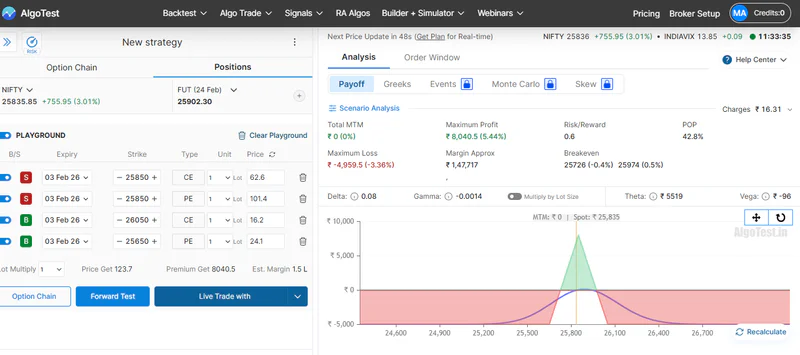

Before choosing a butterfly construction, many traders compare the payoff, margin impact, and risk characteristics of each version using AlgoTest's Strategy Builder. Seeing the structures side by side often makes the differences much easier to understand than reading about them in theory.

Sign up and try free backtesting

Max Profit, Max Loss, and Breakeven

For a standard long butterfly with strikes A (lower), B (middle), and C (upper), equally spaced:

Max profit = (B minus A) minus net premium paid, realized if the underlying expires exactly at strike B

Max loss = net premium paid, realized if the underlying expires at or beyond strike A or strike C

Lower breakeven = A + net premium paid

Upper breakeven = C minus net premium paid

For an iron butterfly (the credit version), the math flips: max profit is the net credit received, and max loss is the difference between strikes minus that credit.

Related: 5 Best Strategy Builders for Options Trading in India (2026)

When Does a Butterfly Spread Make Sense?

A butterfly isn't a directional bet. It's a volatility bet. Specifically, it profits when realized volatility comes in lower than what the options market is pricing in. You're saying: "I think this stays in a range, and the market is overpricing the chance that it doesn't."

It tends to make sense when:

You expect the underlying to consolidate near a specific level into expiry

Implied volatility is elevated, which is common ahead of events like the Union Budget, RBI policy announcements, or major quarterly results, and you expect IV to cool off as the event passes

You can enter at a favorable risk-reward ratio. Many traders look for setups where potential reward is roughly 1:3 or better relative to risk

You want defined risk on both sides, with no chance of an unlimited loss

It tends to not make sense when you have a strong directional view, since the structure is specifically built to be neutral and caps your upside even if you happen to be right about direction.

Check out the 10 Best Algo trading Softwares in India (Free & Paid)

Butterfly vs. Iron Condor vs. Straddle

It's easy to confuse a butterfly with other range-bound strategies, so here's the quick distinction:

Iron condor: Similar tent-shaped payoff, but with a flat top instead of a peak. Wider profit zone, lower max profit per point

Short straddle: Unlimited risk if the market moves sharply, unlike a butterfly's capped loss

Iron butterfly: Functionally the same payoff as a regular butterfly, just built for a credit instead of a debit, using both calls and puts

If you're choosing between these, the real question isn't which one looks better on paper. It's which one fits your view on how wide you expect the range to be, and how much capital you're willing to commit to find out.

Check out AlgoTest documentation to learn more about Option trading strategies

The Real Question: Should You Even Use a Butterfly Here?

Most of the decision-making around butterflies has very little to do with which of the four constructions to use, and everything to do with a more fundamental question: does this market environment actually support a range-bound, low-volatility trade right now?

That's not something you can answer by reading a definition. It's something you answer by looking at how NIFTY, BANKNIFTY, or SENSEX have actually behaved around similar conditions, including IV levels, time to expiry, and recent realized volatility, and how a butterfly structure would have performed across those conditions historically.

Compare Butterfly Constructions Before You Trade

Understanding that all four butterfly constructions have similar expiry payoffs is one thing. Knowing which version works best for your trading style is another.

The differences in capital requirements, margin usage, and risk characteristics only become clear when you test them on real market data.

Instead of choosing a structure based on theory alone, you can compare different butterfly constructions using AlgoTest's Strategy Builder.

With AlgoTest, you can:

Build all-call, all-put, and iron butterfly strategies without coding

Compare payoff diagrams side by side

Backtest different constructions on historical NIFTY, BANKNIFTY, SENSEX, or stock option data

Analyse metrics such as win rate, drawdown, and consistency across multiple expiry cycles

Forward test/paper trade strategies before deploying real capital

This makes it easier to answer the question that matters most: not whether a butterfly strategy works in theory, but which butterfly construction works best for your market view and risk profile.

Related: Options Trading Strategies

Key Takeaways

A butterfly spread is a defined-risk, market-neutral strategy built from three equally spaced strikes, combining a bull spread and a bear spread

All four constructions (all-call, all-put, iron butterfly, and the mixed debit version) pay off nearly identically at expiry, a direct result of put-call parity

The real differences show up before expiry: capital efficiency, margin, and early exercise risk vary meaningfully across constructions

Butterflies work best when you expect low realized volatility and a range-bound move, not when you have a directional view

Understanding the strategy on paper and knowing how it performs in real market conditions are two different things. Backtesting closes that gap

Join AlgoTest as we simplify algo trading for Indian Retail Traders.

This article is for educational purposes only and does not constitute investment, financial, or trading advice.