5 Best Options Backtesting Platforms in India (Free & Paid Compared)

The best free options backtesting platforms in India are AlgoTest, Opstra Definedge, Sensibull, Streak, and Python with NSE data. Each lets you test options strategies on historical NSE data before risking real capital.

Why backtest? The market doesn't care about your logic and most traders find this out the expensive way.

Backtesting lets you pressure-test an idea on years of historical data before you commit real margin. The best part? Several platforms let you do this for free.

Here's what each tool offers and where it falls short.

Options Backtesting Platform Comparison

Key Takeaways from Comparison

Algotest & Opstra → Best free tools for options-specific backtesting

Sensibull → Great for learning, not full testing

Streak → Better for execution than analysis

Python → Maximum flexibility, but requires effort

If you're just starting out and want one tool to begin with, AlgoTest covers the most ground for free before you need to consider upgrading anything.

Related: How to Backtest Algo Trading Strategies: Intraday, BTST, Positional & More

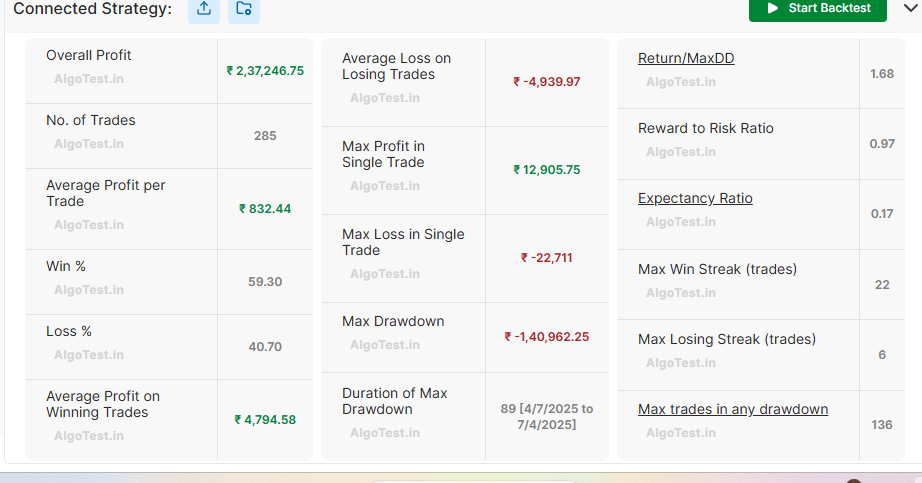

1. AlgoTest

Built specifically for options traders and algo trading in Indian markets, this is one of the most complete tools if you want to backtest without coding.

What you can do:

Backtest multi-leg strategies (straddles, strangles, iron condors)

Select strikes using delta, ATM offset, or fixed levels

Set time-based entries and exits

View detailed trade logs, drawdown, and performance metrics

Can backtest indicator-based strategies on Signals AI

Why traders use it:

You get serious backtesting capabilities without needing technical skills.

Limitation:

The free plan has limits on the historical range and daily runs

Best for: Traders who want structured options backtesting without complexity

2. Opstra

A strong mix of strategy analysis and backtesting.

What you can do:

Test common strategies like straddles and iron condors

Analyze payoff and volatility

Run tests across expiry cycles

Why traders use it:

Good for validating ideas before executing them elsewhere.

Limitation:

Limited historical data in free plan

Best for: Cross-checking and strategy research

Related Read: AlgoTest vs Opstra

3. Sensibull

If you're new to options, this is one of the easiest tools to start with.

What you can do:

Build strategies visually

View payoff graphs and breakeven points

Understand risk before trading

Why traders use it:

Simple interface, easy learning curve.

Limitation:

Full backtesting requires a paid plan

Best for: Beginners

Related: AlgoTest vs Sensibull

Sensibull vs Opstra: Features, backtesting and best platform

4. Streak

More focused on automation than deep backtesting.

What you can do:

Create rule-based strategies

Backtest equities and futures

Deploy directly to broker

Important note:

Options backtesting is limited compared to dedicated tools.

Limitation:

Not ideal for serious options strategy testing

Best for: Traders moving toward live algo execution

Related: Streak vs AlgoTest: Head to Head Comparison

5. Python + NSE Data (DIY)

This is the most flexible option — but requires effort.

What you can do:

Build fully custom strategies

Use libraries like pandas or backtrader

Work with NSE Bhavcopy data

Important note:

NSE data is end-of-day (EOD)

Not suitable for intraday strategies

Limitation:

Requires coding + data cleaning

Best for: Advanced traders and developers

Related read:How to read Options data on AlgoTest

What Is Options Backtesting?

Options backtesting means taking a trading strategy and running it against historical price data to see how it would have performed in the past.

Think of it this way: you want to sell a Bank Nifty straddle every Monday at 10:15 AM and exit it at 3:15 PM. Before you risk ₹50,000 of margin on this, wouldn't you want to know if this idea made money over the last two years? Backtesting answers exactly that.

It's not a crystal ball - past performance doesn't guarantee future results. But it does help you avoid strategies that have a clear structural problem. If a strategy loses money 80% of the time historically, that's a big red flag.

Related read:9 Steps to Build an Algo Trading Strategy from Scratch

How Options Backtesting Works (Step by Step)

Here's the basic process, whether you're using a platform or building something yourself:

Pick your strategy — For example: Sell Nifty 50-delta call + put on expiry day, exit at 50% profit or 2x loss.

Define the rules clearly — Entry time, strike selection method, exit conditions, position sizing.

Feed in historical data — The platform pulls past NSE options data (open, high, low, close, OI for each strike).

Run the simulation — The tool goes through the historical period day by day and applies your rules.

Read the results: win rate, average profit/loss per trade, max drawdown, Sharpe ratio.

Refine the strategy — Adjust and re-test. Don't overfit to past data.

The tricky part with options (compared to stocks) is that each expiry has hundreds of strikes, and the data requirements are massive. This is why quality historical options data is expensive and why truly free platforms often have limitations.

Related: Best backtesting software for Options Trading

Key Benefits of Backtesting Options Strategies

Reduces costly mistakes — You find the flaws before real money is involved

Builds confidence — When you know a strategy has worked historically, you're less likely to panic-exit during a drawdown

Helps compare strategies — Test a Nifty strangle vs. an iron condor on the same historical period and pick the one with better risk-adjusted returns

Speeds up learning — You can simulate years of trading in hours

Real-World Use Case: India-Based Scenario

Say you've heard about the "sell Nifty straddle on Thursday morning and exit before Friday expiry" approach. Instead of putting ₹1.5 lakh of margin on the line and hoping for the best, you run a backtest on Algotest for the last 52 weekly expiries.

The results show:

38 profitable trades, 14 losing trades

Average profit: ₹4,200 per lot

Three trades with losses exceeding ₹15,000

Maximum drawdown during a high-volatility period: ₹42,000

Now you have actual data. You can decide whether to add a stop-loss, reduce position size during high-VIX weeks, or drop the strategy entirely. That's the real value, not guessing, just testing.

Related read: 5 Mistakes Traders Make in AlgoTrading

Risks and Limitations in Backtesting

Backtesting is useful but it's not perfect. A few things to watch out for:

Survivorship bias — Historical data may not include illiquid strikes that were hard to trade in real-time

Execution gap — Your backtest assumes perfect fills. In reality, slippage on options can be significant, especially on deep OTM strikes

Overfitting — If you tweak your strategy too many times to fit past data, it may fail completely going forward

Data quality — Free data sources sometimes have gaps or errors. Always sanity-check your backtest results

Greeks don't backtest perfectly — Theta decay, IV changes, and skew shifts are hard to model accurately in simple backtesting tools

Related: Try Free Backtesting

Backtest Options Strategies with AlgoTest

Serious traders don’t guess, they test first. Backtesting helps you validate a strategy before using real capital.

If you trade NSE options (Nifty, Bank Nifty, FinNifty, etc.), AlgoTest gives you a complete workflow:

strategy → backtest → paper trade → live deployment

For AlgoTrading, read this [comparison of the best algo trading platforms in India]

Why use AlgoTest

No-code strategy builder [step-by-step guide]

Multi-leg backtesting with 7.5+ years of NSE data

Compare strategy variations side-by-side

Realistic results (includes slippage & costs)

Paper trading + live deployment (60+ brokers)

Covers 6 indices + 500 stock options

Clear performance analytics

Pricing: Starts at ₹499/month

Best for: Traders who want a simple, full test-to-deploy setup.

Additional Resources

Trading Tools