How to Backtest Indicator Strategies Before Going Live

You built a trading strategy. Maybe it looked great on a few charts, or maybe it worked well in a handful of recent trades.

The problem is that a few good trades do not tell you whether a strategy actually works. Many traders go live too early, only to discover that their strategy struggles when market conditions change.

That is where backtesting comes in. It shows you how your strategy would have performed on historical data before real money is on the line.

This article explains what backtesting indicator strategies involve, what metrics you should focus on, common mistakes to avoid, and how to backtest trading signals using AlgoTest.

What Is Indicator Strategy Backtesting?

When you trade using technical indicators, your entry and exit decisions come from those indicators. Common examples include RSI, MACD, Moving Averages, EMA, VWAP, Bollinger Bands,ADX and SuperTrend.

Indicator strategy backtesting is the process of applying those trading rules to historical market data to see how the strategy would have performed in the past.

Instead of guessing whether a signal works, you can test it against real market conditions.

For example, you might create a strategy that:

Buys when RSI falls below 30

Exits when RSI rises above 60

Or:

Buys when the 20 EMA crosses above the 50 EMA

Exits when the crossover reverses

A backtest runs these rules on historical data and shows the results. This helps you evaluate whether the strategy has a real edge before risking capital.

For options traders, this matters even more. Options strategies are sensitive to volatility, time decay, and strike selection. A strategy that looks profitable on a chart can behave very differently in live markets.

Related: How to Backtest Algo Trading Strategies: Intraday, BTST, Positional & More

Why Backtesting Indicator Strategies Matters

Many traders skip backtesting because they want to start trading quickly.

The problem is that live trading becomes much more expensive when you are testing ideas with real money.

A proper backtest helps you:

Check whether your strategy has an edge across a large number of trades

Understand how it performs during different market conditions

Measure potential drawdowns and losing streaks

Compare multiple trading signals before choosing one

Build confidence in your trading plan

A backtest cannot predict the future. What it can do is help you make decisions using data instead of assumptions.

Key Metrics to Look at in Your Backtest Results

When reviewing a strategy, many traders focus only on total profit.

That is a mistake.

A profitable strategy can still be difficult to trade if the drawdowns are too large or the risk is too high.

These are the metrics that deserve your attention.

Win Rate

This is the percentage of trades that closed in profit.

A high win rate looks attractive, but it does not guarantee a profitable strategy.

Many successful strategies have modest win rates but strong risk-reward ratios.

Risk-Reward Ratio

This compares your average winning trade to your average losing trade.

A strategy with a 2:1 risk-reward ratio earns two units for every one unit risked.

The higher this number, the less dependent you are on maintaining a high win rate.

Maximum Drawdown

Maximum drawdown measures the largest decline from a peak before the strategy recovered.

This is one of the most important risk metrics because it shows the worst period you would have experienced while trading the strategy.

Average Profit and Loss Per Trade

Review how much the average winning trade generates compared to the average losing trade.

This helps you understand whether the strategy's economics make sense over the long term.

Winning and Losing Streaks

Every strategy experiences periods of consecutive wins and losses.

Knowing these streaks helps you set realistic expectations and avoid abandoning a strategy during temporary rough patches.

Check out 5 Best Indicators for Intraday Trading

Year-Wise Returns

Looking at total profit alone can be misleading.

Year-wise returns show whether the strategy performed consistently across different market environments.

Cumulative PnL vs Underlying

This compares your strategy's performance with the underlying asset or index.

It helps you understand whether the strategy is genuinely adding value or simply benefiting from a strong market trend.

Related Read: [Backtest comparison on AlgoTest]

Common Backtesting Mistakes to Avoid

Backtesting is powerful, but only if done correctly.

These are some of the most common mistakes traders make.

Overfitting the Strategy

Overfitting happens when you keep tweaking settings until the backtest looks perfect.

The strategy ends up fitting past data rather than capturing a repeatable market behaviour.

As a result, performance often collapses in live markets.

Using Too Few Trades

A strategy tested over 20 or 30 trades does not provide enough evidence.

The larger your sample size, the more reliable your conclusions become.

Ignoring Costs

Brokerage charges, taxes, and slippage can significantly reduce profitability.

Always account for trading costs when evaluating results.

Testing Only One Market Condition

A strategy that works in a trending market may fail in a sideways market.

Review performance across multiple years and market environments.

Related Read: [Top Trading Mistakes New Traders Make]

How to Backtest an Indicator Strategy Step by Step

The goal of backtesting is simple.

You create a set of trading rules, apply them to historical data, and analyse the results.

The process generally looks like this:

Define your entry and exit conditions.

Select a historical testing period.

Run the strategy on historical data.

Analyse performance metrics.

Refine the strategy if necessary.

Forward test before going live.

If you are doing this manually, the process can take hours.

This is why many traders use dedicated strategy backtesting software to automate testing and performance analysis.

How to Backtest Trading Signals with AlgoTest

AlgoTest allows you to create indicator-based signals, connect them to options strategies, and run historical backtests without writing code.

If you are looking for a simple way to backtest trading signals, the Signals Backtest feature lets you create, test, and analyse strategies from a single dashboard.

Related Read: [How to Build Indicator-Based Signals with Signals AI]

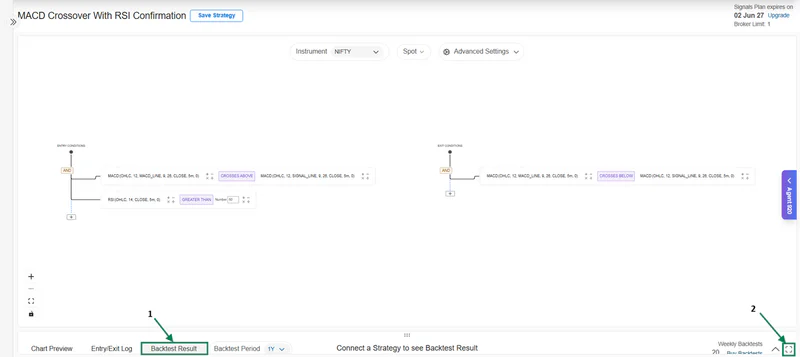

Step 1: Open BackTest Result

After setting up your signal strategy, click BackTest Result.

Use the Maximise option if you want a full-screen view.

Step 2: Connect a Strategy

Click Connect Now.

You can either:

Create a new strategy

Use an existing strategy from your AlgoTest account

Step 3: Build Your Strategy

Click Create Strategy to open the Strategy Builder.

Under Index and Timings, select:

Index

Strategy Type, Intraday or Positional

Entry Time

Exit Time

In the Leg Builder, configure:

Segment

Expiry

Lots

Position

Option Type

Strike Criteria

Strike Type

After completing the setup, click Add Leg.

You can also configure:

Target Profit

Stop Loss

Simple Momentum

For advanced risk management, use:

Overall Stop Loss

Overall Target

Lock Profit

Trail Stop Loss to Entry Price

Click Save and Continue once the strategy is ready.

Related Read: [Signals AI Backtest Documentation]

Step 4: Run the Backtest

Select your preferred backtest period.

Then click Signal BackTest.

The platform will process the historical data and generate performance reports.

Step 5: Read the Results

AlgoTest provides a detailed view of strategy performance.

You can review:

Year-wise Returns

Cumulative PnL vs Underlying

Maximum Drawdown

Monte Carlo Analysis

Total Profit and Loss

Number of Trades

Win Rate

Risk-Reward Ratio

Winning and Losing Streaks

DTE and Weekend Filter Performance

Downloadable Trade Logs in CSV Format

Related Read: [How to Analyse Backtest Reports]

Step 6: Refine and Save

Review the results carefully.

If needed, adjust your rules and run another backtest.

Once you are satisfied with the performance, save the strategy and prepare it for forward testing or live deployment.

What to Do After the Backtest

A good backtest is the beginning, not the finish line.

Before risking capital, run the strategy in a forward testing (paper trading) environment and monitor how it performs in real-time market conditions.

Start with smaller position sizes.

Track whether live performance remains consistent with your backtest expectations.

Review the strategy periodically because market conditions evolve over time.

Related Read: [Algo Trading step by step guide]

The Takeaway

Creating a trading signal is easy.

Knowing whether it actually works is the hard part.

Backtesting indicator strategies helps you evaluate performance, understand risk, and identify weaknesses before you trade with real money.

Instead of relying on assumptions, you can use historical data to make informed decisions.

If you want to create, backtest, and analyse trading signals without coding, AlgoTest's Signals Backtest feature provides a simple workflow to test your ideas before going live.

Join us as we simplify algo trading for indian retail traders.