What is the Impact of Slippage on an Algo?

What is the Impact of Slippage on an Algo?

When evaluating Algos on AlgoTest, it's crucial to understand one subtle but powerful factor that can influence your real-world returns: slippage. While it may sound like a small technical detail, slippage can meaningfully impact how an algo performs when deployed live. Let's walk through what it means, why it happens and how AlgoTest helps you account for it properly.

What is Slippage?

Simply put, slippage is the difference between the price you intended to buy or sell at and the actual price at which your trade gets executed.

For example, imagine an RA Algo signals a buy at ₹500 for a stock. But by the time your order hits the market, the price has moved slightly and you end up buying at ₹502. That ₹2 difference is your slippage.

Similarly, if you wanted to sell at ₹1000 but your order gets filled at ₹998, you faced a negative slippage of ₹2.

While slippage amounts may seem minor on a single trade, they add up significantly over hundreds or thousands of trades, which is typical in systematic trading.

Related: What is Basket Trading

What Causes Slippage?

Several factors contribute to slippage, and they often interplay with one another:

Market Volume and Liquidity: If the stock or instrument you're trading doesn't have enough buyers and sellers available at your target price, your order may "walk the book," meaning it gets filled at worse prices.

Order Size: Larger orders can move the market themselves, especially in less liquid instruments. When many contracts or shares need to be filled, the execution price can slip.

Latency: Even though AlgoTest is designed for fast execution, there will always be slight delays due to internet speed, broker routing, and exchange processing.

Market Volatility: In fast-moving markets (like around news events or during opening/closing minutes), prices can change rapidly. Even a few seconds' difference can create noticeable slippage.

Understanding these factors helps set realistic expectations when analyzing any RA Algo's backtested or live results.

How AlgoTest Helps: Manual Slippage Adjustment

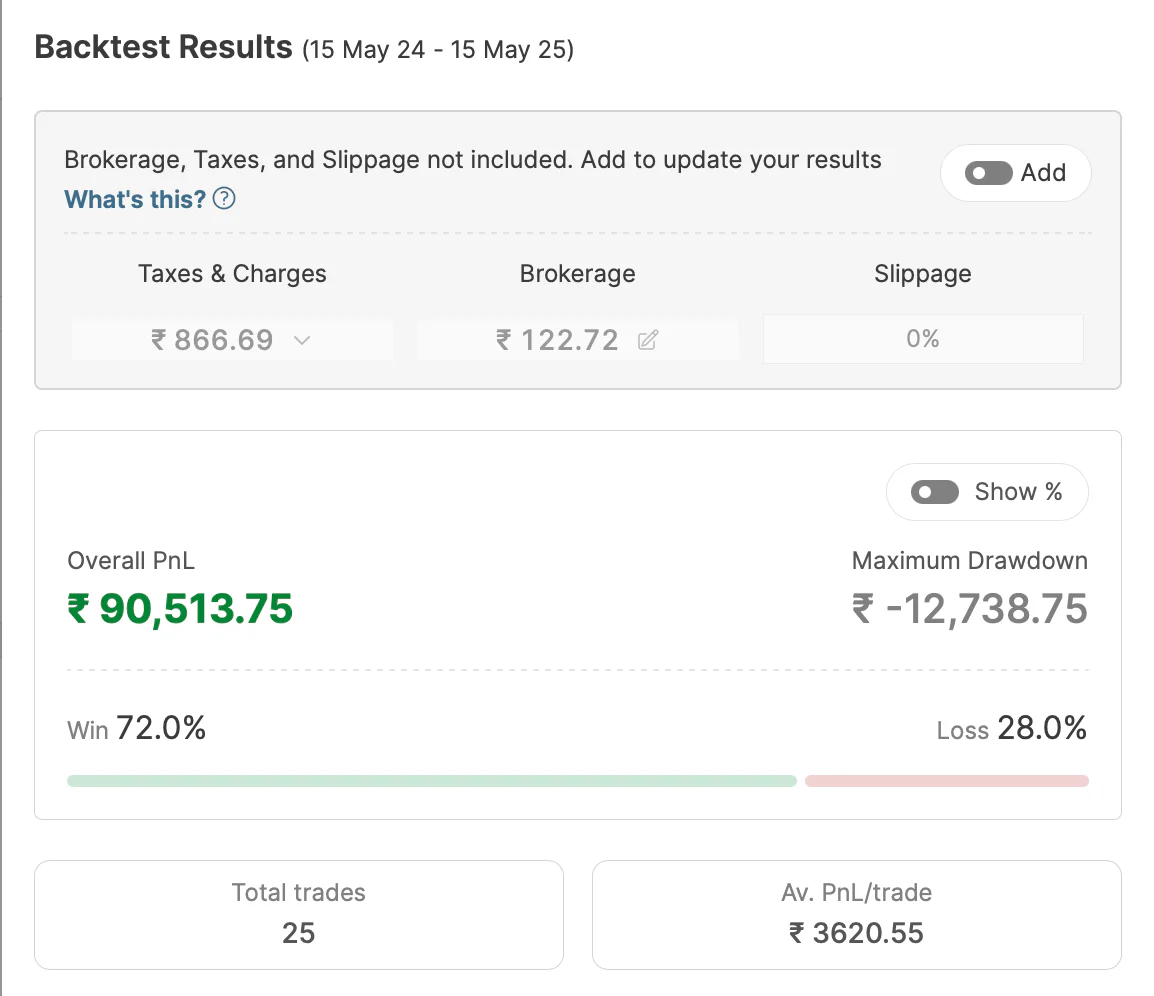

AlgoTest takes slippage seriously. That's why, when you review or backtest an RA Algo, you have the ability to manually input a slippage estimate.

This simple yet powerful feature lets you:

Simulate more realistic trading conditions.

Avoid overestimating potential returns.

Understand the robustness of an algo even with minor execution inefficiencies.

By entering a slippage value (for example 1% percentage), you can see how the algo's metrics, like returns, drawdowns, and win ratio, would change if you experienced that level of slippage consistently.

Related: What is the Algo Trading Marketplace on AlgoTest

This gives you a much clearer, more conservative view of performance before you decide to deploy live.

Check out the 10 Best Algo trading Softwares in India (Free & Paid)

Conservative vs Aggressive Slippage Estimates

One common question is: "How much slippage should I assume?"

The answer depends on your approach and risk tolerance, but here are some general guidelines:

Conservative Approach:

Assume higher slippage, especially for instruments with lower liquidity or during volatile sessions.

This helps you prepare for worst-case scenarios and reduces the risk of unpleasant surprises.

Example:

Nifty Selling - 0.5% slippages

Nifty Buying - 1% slippages

Sensex Selling - 1% slippages

Sensex Buying - 1.5% slippages

Aggressive Approach:

Assume minimal slippage, betting on optimal market conditions and excellent broker execution.

This can show more optimistic results but carries the risk that real-world performance might disappoint.

Example: For Nifty options with high liquidity, you might assume 0.5-1 percentage slippage.

Tip: When in doubt, lean towards conservative estimates, especially if you're new to algorithmic trading. It's better to be pleasantly surprised than to be caught off guard.

Related: What is Basket Trading

Why Factoring Slippage Matters for RA Algos

Since RA Algos are execution-only, meaning they handle entries, exits, and risk management without disclosing full internal logic, it becomes even more important to:

Trust the research (all algos are by SEBI-registered Research Analysts and vetted)

Prepare for real-world frictions like slippage, brokerage fees, and latency

Slippage directly affects your net profitability. For instance, an algo showing 20% annual return with no slippage might only yield 15% once realistic slippage is factored in. That's a material difference, especially over longer periods and larger capital deployments.

AlgoTest ensures transparency by showing backtested results with all trading costs considered. But your personal slippage experience could still vary depending on broker, internet speed, and market conditions. Always use the manual slippage feature to personalize your expectations.

Related: Why do we need backtesting?

Key Takeaways

Slippage is normal and unavoidable in live trading, but you can plan for it.

Volume, volatility, latency, and order size are key drivers of slippage.

AlgoTest lets you adjust slippage manually during backtesting, helping you model real-world outcomes.

Use conservative slippage assumptions to protect yourself from overly optimistic expectations.

Past performance includes costs, but real-world execution can still differ slightly, always be prepared.

By understanding and proactively accounting for slippage, you'll set yourself up for a more confident, informed trading experience with RA Algos.

Ready to explore? Remember, each RA Algo card on AlgoTest transparently displays the margin requirement, historical drawdown, and other vital metrics, all designed to help you make the best decision for your journey into systematic, research-backed trading.