General FAQs

Here we have tried to answer some common questions about our products: Backtesting, Forward Testing, & Live Execution

Execution

How do I stop a strategy and re-deploy it again if I have activated a wrong strategy?

A user can deploy their strategy anytime after 8:45 am and before market closes on days when the market is open. There are 2 ways where a user can stop a strategy and re-deploy it.

- Stop and re-deploy before market open: To stop any strategy before the market opens (9:15 AM) we have 2 options; Square off or Switch to Manual. They work similarly and stop the strategies. The major difference comes when re-deploying a strategy after stopping one. If the user clicks on "Switch to Manual" their live execution daily limit will be reset immediately and you shall be able to re-deploy your strategy. But if the user clicks on "Square off" their live execution limit shall be reset after 9:15 AM after which they will be able to deploy a strategy.

- Stop and re-deploy after market open: To stop a strategy after market open (9:15 AM), the user can use either " Switch to manual" or "Square off" function to stop a running strategy, provided that no trades have been taken in the said strategy. The daily live execution limit shall be reset immediately and the user will be able to redeploy a different strategy.

- Stop and re-deploy a strategy if a trade is taken: If a trade has already been taken when the user realizes that a wrong strategy has been activated, then the user should use the "Square off" option to square off the the existing trades before activating the correct strategy. The user should keep in mind that a strategy can only be activated if the entry time is a minimum of 2 mins after the current time.

Once I have activated a strategy for live deployment, can I make any changers to it?

No, you will not be able to make any changes to the parameters/conditions of a strategy after it has been activated & deployed. Once you activate a strategy, we save the conditions/parameters associated with that strategy. Any changes that you make to the strategy after it has been activated will not be reflected on your deployed strategy. To make any changes to your deployed strategy, you will first have to stop it by either Squaring off or Switching to manual. Thereafter, you can deploy the newly modified strategy.

Do my Overall strategy settings like Overall Target & Stop Loss change if I use the quantity multiplier to increase by quantity?

The Quantity multiplier multiplies the number of lots in each leg. If your Overall settings e.g. Overall SL, Overall Profit, and Overall TSL, are based on MTM, then they are also multiplied.

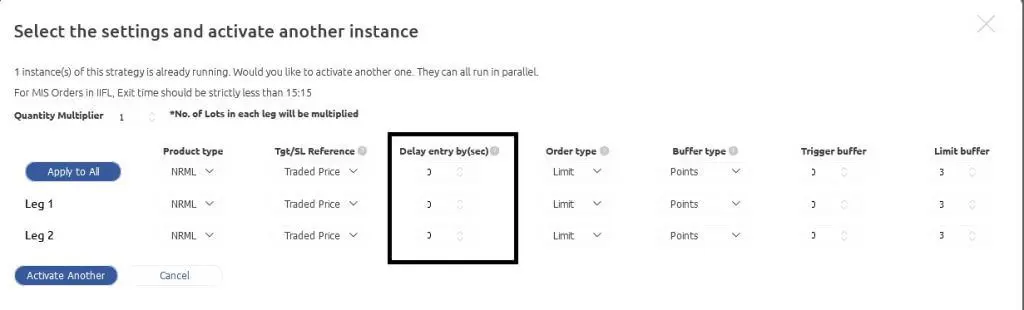

How do I make sure that my sell legs are entered after my buys legs?

Many users buy hedges for margin benefit. In order to make sure that your sell orders are executed after your buy orders and you are able to get the margin benefit, we have added a feature of "Entry Order Delay" in your execution settings. Your execution settings open up as soon as you click on the "Activate" button for a strategy. Under these settings we have given a time dial where you can you can delay the entry of any of your legs by 0 - 50 secs.

Backtesting

When can I backtest today's trades?

Our backtest data is updated usually after 12 am that night, so the beginning of the next day. We go through a rigorous process of checking the data from multiple sources before it is updated to our database.

Why is the lot size not changed in your backtest? Why is it constant?

Yes, this was a conscious design choice. Even though the lot size changed over time, it makes more sense to keep it constant while backtesting using historical data. When evaluating strategies, a Rs 1 move in your favour shouldn't show Rs 25 profit on one day, and Rs 50 profit on some other day, even though market conditions remain the same. Different lot sizes in backtests can obfuscate the signal, so we advise you to keep it constant for the duration of the entire backtest.

Why do you not have any in-built slippages?

This was a design choice - we keep slippages 0 so as not to obfuscate the strategy result. Instead we give the user the ability to add slippage which is closest to the slippages they see in their execution. So you can add whatever slippage you think is appropriate on the backtest results. You can also change the value of slippages and re-calculate your results to see how sensitive your strategy results are to slippages.

What is the difference between the Days of Max Drawdown vs Max trades in a drawdown?

Max trades in a drawdown: Max trades in a drawdown shows the maximum number of consecutive trades your strategy was in a drawdown phase. This drawdown period can be different from the period where your strategy incurred the maximum drawdown (monetarily), which is shown in the first field i.e. Days of Max Drawdown.

Max trades in a drawdown shows the max amount of trades taken to recover any drawdown which may or may not correspond to the maximum drawdown monetarily.