How to Backtest Options Strategies in India (2026 Guide)

Backtesting an options strategy means testing your trading strategy on historical data to see how it might have performed under different market conditions and settings. It helps traders validate ideas, refine rules, and build more systematic strategies before going live and risking real capital.

In this blog, we cover a simple step-by-step workflow to backtest options strategies, common mistakes retail traders make, practical examples, and key best practices.

Why Options Backtesting Is Different from Stock Trading

Backtesting is especially important in options trading because options have more variables than stocks. Factors such as expiry dates, volatility changes, and multi-leg setups can significantly impact how a strategy performs. Testing your strategy first helps you understand what might happen before risking real money.

Key Differences

Multi-leg strategies: Many options strategies involve more than one position at the same time. Backtesting helps you see how all parts of the strategy work together in different market conditions.

Expiry and time decay: Options lose value as expiry gets closer. Testing shows how time can affect your profits and losses.

Volatility impact: Option prices change when market volatility changes. Backtesting helps you understand how your strategy reacts during calm and volatile periods.

Execution matters more: Slippage, liquidity, and order fills can affect options trades more than stock trades, so realistic testing is important.

Step-by-Step Guide to Backtesting an Options Strategy

Backtesting helps you understand how your strategy might perform under different market conditions, indicators, and price movements. While it does not guarantee profitable live trades, it is an important step to validate your strategy and manage risk before going live.

You can check out our product doc for a full walkthrough on backtesting intraday,positional, BTSD, crypto and stock options strategies using AlgoTest.

1. Define Strategy Rules

Before running any backtest, clearly define your strategy. Vague rules lead to unreliable results.

Start by answering:

Entry condition: When should the trade start? This could be a specific time, price level, or market condition.

Strike selection: Decide how you will choose strikes, ATM, ITM, OTM, or based on premium or delta.

Expiry choice: Select weekly or monthly expiry depending on your strategy logic.

Exit or stop-loss rules: Define when to exit the trade. This could include time-based exits, target profit, stop-loss levels, or adjustment rules.

Clear rules ensure that your backtest reflects a repeatable strategy rather than random decisions.

2. Select the Right Historical Period

Choosing the right data range is important for realistic results.

Test your strategy across different market conditions, including trending, sideways, and volatile periods.

Avoid testing only recent bullish markets, as this can give misleading results.

A broader time range helps you understand how your strategy performs in changing environments.

3. Run the Backtest

Once your rules and data are ready, you can run the backtest.

Choose a platform or tool that supports options strategies.

Simulate trades using historical market data.

Review the basic output generated by the system, including trades taken and overall performance.

The goal here is not perfection but understanding how your strategy behaves over time.

4. Evaluate Key Results

Focus on a few essential metrics instead of analyzing everything.

Profit/Loss: Overall profitability of the strategy.

Maximum drawdown: The largest loss period, which shows risk exposure.

Win rate: Percentage of winning trades compared to losing trades.

Consistency: Whether results are stable across different time periods.

Keeping your evaluation simple helps you make better decisions without overcomplicating analysis.

Related: How to Backtest Indicator Strategies Before Going Live

Real Examples of Backtesting Options Strategies

Examples of backtesting strategies will help you understand how these options strategies will work in practice. These examples are for educational purposes to show how a strategy can be set up and backtested. They do not guarantee success in live trades.

Related: How to Backtest Algo Trading Strategies: Intraday, BTST, Positional & More

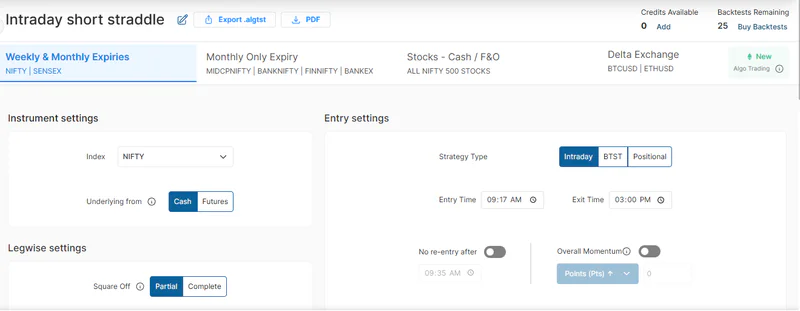

Example 1 — Short Straddle Backtest

A short straddle strategy is used when traders expect the market to stay in a range and not move strongly up or down. In this strategy, a trader sells both a call option and a put option at the same strike price (usually ATM) and the same expiry.

Strategy setup: Sell an ATM Call (CE) and ATM Put (PE) on Bank Nifty or Nifty weekly expiry.

Entry rule (example): Enter the trade at 10:15 AM after initial market volatility settles.

Strike selection: Choose the strike closest to the current spot price (ATM).

Risk management:

Set a stop-loss of around 35%–50% on each leg, or

Use a combined strategy stop-loss of around 1.5x total premium collected.

Exit conditions:

Intraday exit at 3:15 PM, or

Exit earlier if stop-loss triggers.

Key insight from backtesting: Results may look strong during sideways markets, but drawdowns increase during trending days. Testing across multiple months helps identify this behaviour.

AlgoTest allow traders to quickly simulate these rules

Example 2 — Iron Condor Backtest

An iron condor is a defined-risk strategy designed for range-bound markets.

Strategy setup:

Sell an OTM call spread and an OTM put spread.

Example: Sell +/- 200 to 300 points away from spot price depending on volatility.

Entry rule (example): Enter between 10:00 AM – 11:00 AM once market direction becomes clearer.

Risk management:

Defined risk due to hedge legs.

Strategy-level stop-loss around 1.5x–2x premium received.

Exit conditions:

Exit at 70–80% profit target, or

Close at expiry day afternoon to avoid gamma risk.

Key takeaway: Backtesting helps identify optimal spread width and strike distance for better consistency.

Example 3 — Short Strangle Backtest

A short strangle gives more room for price movement compared to a straddle by using out-of-the-money strikes.

Strategy setup: Sell OTM call and put options.

Strike selection example: Choose strikes with premium around ₹40–₹60 or delta near 0.15–0.20.

Entry rule: Enter around 10:30 AM or when implied volatility is elevated.

Risk management:

Stop-loss of 40%–60% on each leg, or

Adjust position if price moves within 50–75 points of strike.

Exit conditions:

Intraday exit at 3:15 PM, or

Hold until weekly expiry depending on strategy.

Key insight: Backtesting often shows higher win rates compared to straddles but lower premium collection, highlighting the risk vs reward trade-off.

AlgoTest’s Backtester makes it easier to test different timings, stop-loss levels, and strike distances quickly and compare results across historical data.

Common Mistakes Retail Traders Make When Backtesting Options

Many retail traders make mistakes that lead to unrealistic expectations. Avoid these common errors during backtesting to get a realistic picture of your strategy.

Choosing automation without validation: Many traders focus only on automating a strategy without properly testing it first. Automation should come after you confirm that the strategy works across different scenarios.

Testing only one market condition: Running a backtest only during bullish or low-volatility periods can give misleading results. Strategies should be tested across trending, sideways, and volatile markets.

Unrealistic slippage assumptions: Ignoring execution factors like slippage, liquidity, or order fills can make backtest results look better than real trading outcomes.

Overfitting historical data: Adjusting rules repeatedly just to improve past performance may create a strategy that looks good on paper but fails in live markets.

Ignoring risk management: Focusing only on profit without analysing drawdowns or loss periods can lead to strategies that carry excessive risk.

Simple Workflow for Backtesting Options Strategies Using AlgoTest

Bactesting becomes easier when you follow a structured workflow. AlgoTest provides a one-stop solution to build a strategy, backtest and analyse and compare reports.

Create strategy: Define the structure of your strategy, including legs, entry timing, strike selection, and expiry type.

Set rules: Add conditions such as entry time, stop-loss levels (for example, 35%–50% per leg), target exits, or adjustment logic.

Run backtest: Execute the strategy on historical market data to simulate trades across different market conditions.

Analyse report: Focus on a few key metrics to understand performance:

Profit/Loss: Overall returns generated by the strategy.

Maximum drawdown: Largest decline in capital, showing risk exposure.

Win rate: Percentage of profitable trades.

Consistency: Stability of results across different time periods.

Risk-to-reward behaviour: Whether profits justify potential losses.

Iterate: Adjust parameters such as strike distance, entry timing, or stop-loss rules and re-run the backtest to improve results.

This structured approach helps traders validate strategies before moving to automation or live execution.

Backtesting Options Strategies with AlgoTest

Options strategies have many moving parts like multiple legs, expiry, and volatility. Backtesting helps you test different setups, track key metrics, and understand how the strategy performs in real market conditions.

AlgoTest provides built in tools that help you backtest your strategies with different indicators, filters, multiple time periods and real world costs.

Some of our key features include:

Visual Strategy Builder - AlgoTest allows traders to create multi-leg options strategies using a visual interface, making it easier to test spreads, straddles, condors, and other complex setups without coding.

Backtest Comparison feature -This feature helps you compare your strategies across different metrics to help you optimize your strategies

Leg-Wise Risk Controls - Traders can define stop-loss levels, entry timing, and strategy rules to see how execution assumptions impact results, which is especially important for options trading.

Signals AI for Indicator-Based Strategy Creation– Build options strategies using technical indicators and test them quickly without manually defining every condition.

Portfolio Backtesting - AlgoTest allows users to backtest multiple strategies together and compare results side-by-side to understand diversification and consistency.

Margin Estimate Feature - With this tool, you can confidently proceed with your strategy without any worries about meeting margin requirements of your brokers.

Make sure to follow these simple steps during bactesting your trading strategies

Define clear entry, exit, and risk management rules.

Choose the right historical period and test across different market conditions.

Simulate trades using a reliable options backtesting platform.

Focus on key metrics like profit/loss, drawdown, win rate, and consistency.

Adjust parameters and repeat testing to refine the strategy.

Start your algo trading India journey with AlgoTest and get 25 free backtests every week.