Leverage in Trading: Futures Contracts

Furthering our theme of 'leverage in trading’ from the last blog post.

This article will introduce the application of leverage in the FnO segment. We’ll start with futures.

Let's first define the concept of “notional exposure”.

Notional exposure or notional value can be thought of as the total amount of the underlying instrument(s) that your position controls. What does this mean? Let's calculate the notional value of a futures trade as an example:

To buy one lot of Adani Enterprises futures, margin required = Rs 1,00,915

Calculate this here on Margin Calculator.

This gives you control of 250 shares of Adani Enterprises as the minimum lot size is 250 shares.

The notional value in this case is 250*1770 = Rs 4.4L

So, Notional Exposure = Contract Size x Spot Price

Now how is this notional value related to the amount of margin required?

As you can see, when trading a futures contract, you have to pay a significantly lesser margin to achieve control of a certain number of shares as compared to buying the stock. This is leverage, and the ratio in this case is 4:1 or 4 times.

So, leverage = notional exposure / margin required

Unlike the example from our previous article, you don’t need to borrow money to have a leveraged position. Hence, buying a futures contract by design gives you leverage!

Why is this important?

As discussed in the previous article, leverage juices up your return if you’re correct, but can really hurt if you’re wrong.

Notional value is an important concept to grasp as a trader, because it helps you understand how leveraged you are. The more leveraged you are, the higher the risk if the position goes against you.

We'll spend a lot more time talking about notional value in the days to come, but first let's answer the burning question:

How do you use Notional Exposure to Determine your Risk?

This is much easier to illustrate with an example.

Remember, Notional Exposure = Contract Size x Spot Price

In the Adani example above, the notional value is approximately Rs 4.4L for 1 lot of an Adani Enterprises futures contract. This means, that if the stock went to 0 for whatever reason, the most you'd lose is NOT just the Rs 1L you paid in margin, but you would ALSO OWE your broker Rs 3.4L.

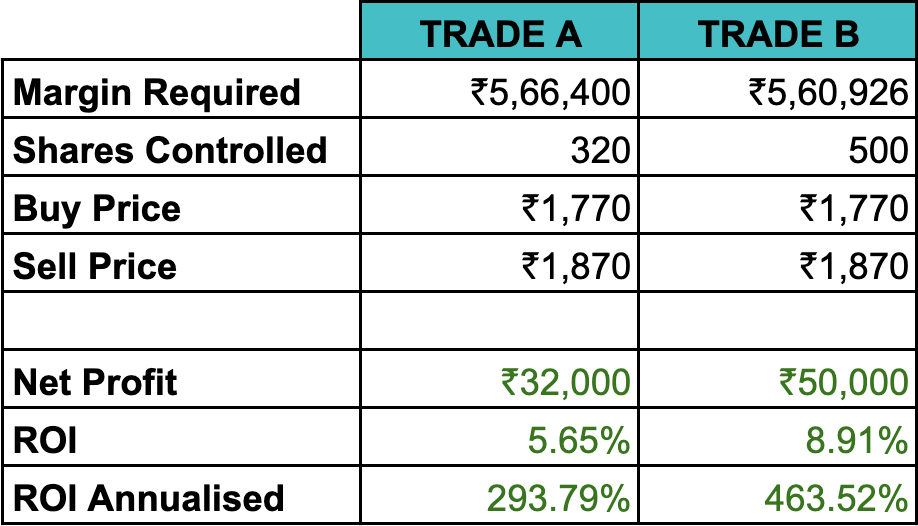

To illustrate the magnitude of risk that is possessed by over-leveraging, let's take two types of trades on Adani Enterprises with a 6L account utilising roughly the same margin for both cases.

Trade A: Buy 320 shares of Adani Enterprises = Margin of Rs 5.6L

Trade B: Buy 2 Adani Enterprises futures contracts = Margin of Rs 5.6L

Case 1: Adani Enterprises Rises by Rs 100 in 1 week

What would our P&L look like in both trades if the stock rose by Rs 100 in both trades?

Evidently, your ROI and hence annualised ROI is significantly higher when trading the futures contract instead of buying the stock.

Case 2: Adani Enterprises Falls 70% in 1 week

Hindenburg Research published a (perhaps telling) report on the Adani group and their alleged "con” on the 24th of January, 2023. The aftermath resulted in Adani stocks hitting lower circuits, with Adani Enterprises falling 70% in the span of a week between 25th Jan & 3rd Feb 2023.

PS: you can read the report here: https://hindenburgresearch.com/adani/

In this scenario, what would our P&L numbers look like?

Quite the blood-bath in both cases, but I think you can clearly see leverage at play on the downside, too.

In Trade B, not only would you lose the entire Rs 6L of capital in your trading account, you would now ALSO OWE your broker Rs 20,000!!

This, is why position sizing is key, and using notional exposure to position size is a great place to start. A 1X notional exposure is a decent starting point for those new to trading.

However, you can trade with more than a 1X exposure even as a newbie, provided you sell ‘courses’ to offset your trading losses 😉😉

https://giphy.com/gifs/fazeclan-faze-clan-fazeup-hR0A1kHhm61XhJKahb

POV: You start trading a furu's 'No Loss' strategy 🤠

NOTE:Marked-to-market settlements in futures trading happens at the end of each day. In Trade B from above, the risk management mechanisms of the broker and the exchange would have resulted in margin calls in one's account. This would require you to furnish more capital in your trading account, or your positions would be squared off. For the sake of simplicity, however, we have disregarded this clearly illustrate the effect of leverage.