Leverage in Trading: Short Options

We've explored leverage in an IPO, futures and long options. To conclude this series (for now, anyway), let's discuss how leverage works when you are short options. Check out all our other blogs here.

How are you leveraged as an option seller?

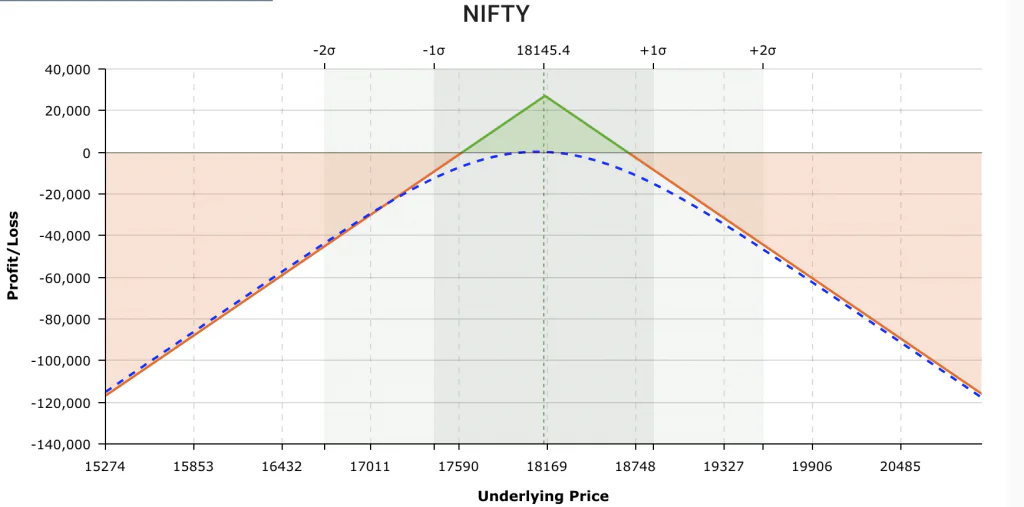

Let's understand this with the help of one of the most famous trading strategies on FinTwit and our AlgoTest platform; the short straddle. We will demonstrate using the Nifty 50 index.

Trade details-

Nifty Spot - 18150

- sell CE 18150 @ Rs. 304

- sell PE 18150 @ Rs. 238

The payoff for the same is given below.

Max profit = premium received = Rs. 27,100

Max loss = unlimited

Why is your loss unlimited you ask? Well, the underlying could (theoretically) appreciate to any level, or it could go to zero. If the underlying moves a large amount in either direction, it could result in an MTM loss even higher than the amount of margin money you deposited with your broker! In this case, you'll definitely get a margin call from your broker!

You will need to add more funds in your account to carry on the position, or else the broker might square off your positions and potentially charge a penalty.

Notional Value

Leverage, as you can remember, allows one to use a small amount of money to theoretically control a much larger position. This much larger position is nothing more than the notional value we discussed in this blog. It is the total underlying value that can be controlled by your option position. Thinking in terms of this notional value helps differentiate between the total value of a trade from the cost of taking the trade.

The notional value of a short option is calculated as (Strike Price - Premium) * Lot Size

The notional value in the case of a short straddle is calculated slightly differently. This is because only one side will be tested in the case of a straddle and not both.

NV = (spot price) x (lot size)

From our example, the notional value is (18150 x 50) = 9L approx.

Different Leverage Scenarios

Back to the strategy, the margin in your trading account required to trade 1 lot of this strategy is approximately 1.8L.

Therefore, if our capital base was 2L, we would be trading at a 4.5X notional exposure (9L / 2L). If we were to trade this strategy with a 2L account, the most we would stand to lose in a lower circuit intraday (index moves up or down by 20%) would be 1.5L or 75% of your account!

Lets lower this potential loss by using notional value to determine position sizing.

Using notional value to determine our position sizing, if we traded at a conservative multiple of 1X (no leverage) this time, we would now need the full 9L to trade one lot. Now, the most we would stand to lose in the event of a circuit would be about 18.5%. Still a large percentage, but a far cry from the 75% witnessed earlier.

To understand leverage and its effects on your P&L in short options even better, let's take another example. Consider an INR 10L trading account. Let's gradually increase the number of lots traded but keep the total capital fixed at 10L. As we increase our lots traded, our leverage also increases, and our losses will be magnified relative to the same move in the underlying index.

From our previous blog posts we can conclude that leverage juices your returns. The table above however, demonstrates that it also carries with it (potentially) insurmountable risk if not thought about or considered appropriately.

There is no absolute right answer to how much leverage one should utilise, but conservative traders could use 1.5 - 2X notional exposure, while more aggressive traders could have 3X or so as their benchmark. Trading with more than 3X exposure will yield higher returns, but in turn, will definitely leave you hanging dry when the market moves against you!

We will expand on this concept in the next blog when we talk about how whether your 'hedges' are really 'hedges'. Stay tuned 😉