Position Size Calculator: How to Use Trading Edge & Kelly Sizing

In the pursuit of consistent profitability, traders often focus intensely on entry and exit rules. However, the true differentiator between a successful long-term trader and one who eventually fails is not the strategy itself, but the rigorous search for a trading edge, and the application of position sizing once the edge is discovered. On the topic of position sizing, traditional position size calculators focus on a fixed percentage of risk per trade, a more advanced approach, which we've embedded in our edge calculator, delves into the mathematical expectation of a trading system, its trading edge, and then the final application of sizing of capital survivability.

This article explores this advanced perspective on position sizing in trading, showing how to quantify your system's edge, simulate its long-term behavior, and use the Kelly Criterion to determine the optimal position size that maximizes growth while protecting your capital.

Quantifying Your Trading Edge: The Foundation of Position Sizing

The first step in advanced position sizing is to answer a fundamental question: Does your trading system have a positive expected value? This value is known as the Trading Edge.

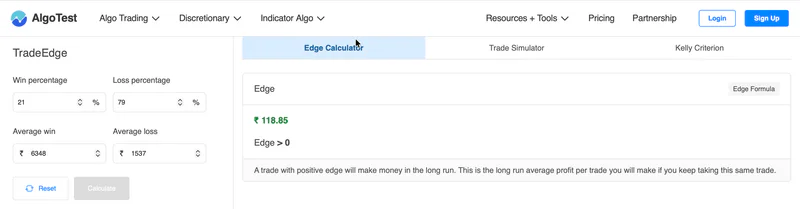

The Trading Edge Formula

The Trading Edge is the probability-weighted average profit per trade over time. It is calculated using the system's historical performance statistics:

Trading Edge = (Win Percentage×Average Win)−(Loss Percentage×Average Loss)

A system with an edge greater than zero is expected to make money in the long run. Conversely, a system with a zero or negative edge, even before accounting for transaction costs, is mathematically destined to fail.

Many retail systems lose not because they’re 'negative edge,' but because they’re zero edge, and costs (brokerage, slippage, taxes) push them below zero.

Positive Edge ≠ Win Every Trade

A crucial insight from the edge calculator approach is that a positive edge does not mean you will win every trade. For example, a highly profitable options buying system might have a Win % as low as 21%, but a high Average Win that more than compensates for the frequent, smaller losses. The position size formula must account for this reality, as long losing streaks are an expected part of the system.

To learn how to use the edge calculator, read the position size calculator documentation here.

The Role of Trade Simulations and Capital Survivability

Even with a quantified positive trading edge, a trader can still fail if they bet too aggressively or start with insufficient capital. This is the concept of capital survivability.

The Risk of Aggressive Sizing

As shown by trade simulations, even a positive edge system can lead to a trader being forced out of the market if their capital falls below the minimum margin required to place the next trade. This occurs when a max losing streak (a series of consecutive losses) is longer than the trader's capital buffer can withstand.

Trade simulations, a key feature of an advanced position calculator, test the system against a large number of hypothetical trade sequences to determine:

Maximum Drawdown: The largest peak-to-trough decline in capital.

Maximum Losing Streak: The longest run of consecutive losses.

These simulations highlight that trading edge alone isn’t enough; you need appropriate position sizing and adequate capital to survive the inevitable losing streaks and realize the long-term edge.

Kelly Sizing: Optimizing Position Size for Growth

To solve the problem of aggressive betting and capital survivability, advanced position sizing utilizes the Kelly Criterion. This formula determines the optimal fraction of capital to bet on a trade to maximize the long-term growth rate.

Full Kelly vs. Fractional Kelly

The Full Kelly size is mathematically proven to maximize the growth rate, but it is often too aggressive for practical trading. It results in extremely high volatility and deep drawdowns, making it psychologically and practically unsustainable, especially when minimum bet sizes (margin) are a factor.

The practical solution is Fractional Kelly (e.g., Half Kelly or 10% Kelly). This method significantly reduces the volatility and maximum drawdown while still capturing a substantial portion of the maximum possible growth. It is the preferred method because it prioritizes capital survivability, ensuring the trader stays in the game, over maximizing short-term returns.

Raghav talks in detail about this concept in his course, you can opt-in his volatility course to learn more about position sizing.

Integrating Traditional Position Sizing and Market-Specific Calculators

While the edge calculator approach provides the optimal capital fraction, the traditional position size calculator is still necessary to translate that fraction into the actual number of units to trade.

The standard position calculation formula for execution:

This formula is adapted for various markets using specialized tools:

By combining the risk-based approach (using the stop loss calculator to define risk per unit) with the advanced edge-based approach (using Kelly Sizing to define the total risk amount), a trader achieves a robust and mathematically sound risk management calculator framework.

Conclusion:

The position size calculator is the ultimate tool for systematic trading. It moves the trader's focus from the unpredictable outcome of a single trade to the long-term, predictable expectation of the system. By understanding and applying the concepts of trading edge, trade simulations, and fractional kelly sizing, a trader ensures they are not trading blind. They are equipped to survive the inevitable drawdowns and remain capitalized to capture their positive edge over the long run.

If you want to understand advanced concepts like Implied Volatility, we have a series of articles explaining IV, IVP-IVR, RV & VRP Analysis.