Forward Testing is now live on AlgoTest! You can now simulate your saved strategies against live market data in real time! What is Forward Testing?

How to Interpret a Backtested Portfolio’s Aggregate Results

This will be a short blog post on interpreting a backtested portfolio’s aggregate results on AlgoTest. Backtesting a Portfolio We released a blog post a

Backtest An Option Buying Strategy Using VWAP

In this blog post, we’ll show you how to backtest an option buying strategy using the VWAP indicator, available exclusively on AlgoTest. A few days

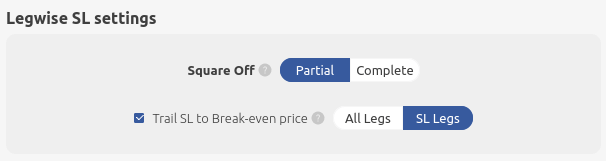

Trail Stop Loss to Break-Even Price when Backtesting

In this post, we’ll show you two variations of the Trail Stop Loss to Break-Even Price when backtesting on https://algotest.in. Building block 1 – Square

Backtest Multiple Strategies Together Using the Portfolio Feature

We recently introduced a new feature on algotest.in called Portfolio, which allows you to backtest multiple strategies together. In this blog, we’ll backtest a sample

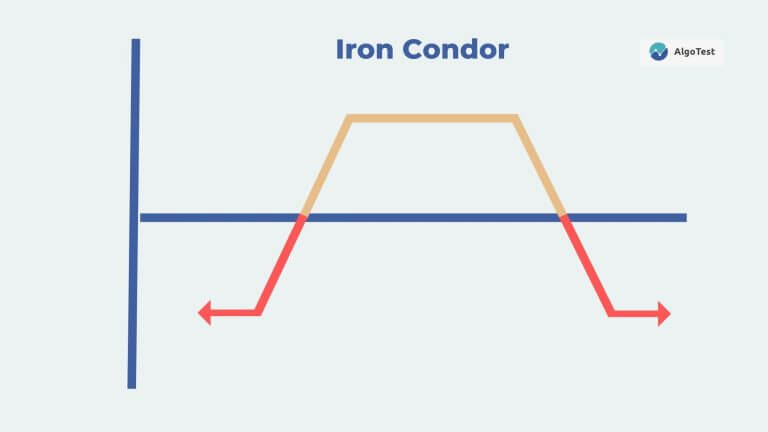

Intraday Iron Condor Built Using Straddle Width

We’d like to introduce a new feature for strike selection on algotest.in, we call it “ATM Straddle Width”. How to get the ATM straddle price?

Why is the backtest loss higher than my Stop Loss? Is it a bug on your platform?

Since we have started AlgoTest.in, we’ve received countless messages from users asking how its possible that their backtest loss higher than stop loss value? Specifically,

How does AlgoTest define a candle?

We recently received an interesting query from a user, which relates to how does AlgoTest define a candle: “On Friday ( 24th Feb 2022) Enter

Why Do We Need to Backtest Trading Strategies in India? What are its limitations?

Before we jump into why we must backtest trading strategies, lets first understand what backtesting is! Investopedia defines it best as: “Backtesting allows a trader